Commissions Vs. Fees

Commissions Vs. Fees

While I am a proponent of No-Load Index investing, I like the Magic Annuity better! This will make sense as we go along. But first let’s talk about COMMISSIONS! Yes, commissions are different than fees. How do they differ?

- Commissions are NOT SUBTRACTED from your principal investment because you are NOT paying the commissions;

- Generally, a commission is paid to the investment advisor one time only on the initial principal investment; and

- While a commission may seem like a lot of money up front (it can be as low as 1% or as high as 9%), YOU NEVER PAY the commission, unless you break your contract early.

The Insurance Company, just like the Mutual Fund Provider or Bank, shares with you in the upside of the market returns. The difference with the MAGIC ANNUITY is that the Insurance Company GUARANTEES your principal investment, pays the up-front commission out of their own pocket, and must wait, often up to 7 years or longer, to get any return on their investment (ROI). In exchange, they require you to stay in the contract long enough for them to recoup their costs and be able to make some return on their investment. During the entire time you’re in the contract they never extract a dime out of your account and continue to credit all returns based on 100% (sometimes more) of your principal. Even if you did need some of your money early, you have so many options like:

- 10% (sometimes more) Penalty Free Withdrawals

- Borrow money out (must qualify)

- Annuitize (select one of usually a dozen options to start receiving pension payments, like guaranteed income for life option or many others)

- Hardships requests

Bonuses and Guarantees

Bonuses and Guarantees

The Magic Annuity often offers BONUSES when you make your initial deposit. Yep, sometimes as high as 10% (if you’re 52 or younger, or 5 to 7% if older)! Imagine, you invest $100,000 in the Magic Annuity, and your first statement shows an accumulation value of $110,000!!! Wow you just made 10% return and all you did was make the initial investment! Now it’s not always 10% maybe its 5%, but that isn’t a kick in the head either!

So, let’s say the Advisor in this case made a 7% commission on your $100,000 investment. The next day your account is credited with an opening balance of $110,000. Hmmmmmm. Would you consider staying with this investment for 5 to 10 years, after which all or most of your penalties disappear? Remember, you have penalty free access, if you need it.

For me, the fact that the Insurance Company is paying the commission out of their pocket and giving me a bonus on my initial investment as well, more than offsets the commitment I need to make, to stay in the product for a few years. Even Certificates of Deposits (CD) at banks will reduce my payout if I withdraw the CD funds early. It is all based on the time value of money. They simply need enough time to create returns high enough to cover the principal, plus bonuses, plus returns on investment, plus the commission. Plus, my Principal is GUARANTEED the entire time. Even if the market crashes I will not only not lose principal, but I will not lose ANY of the gains I made up to that point. More on this later.

On FEE-Based plans the FEES are ALWAYS THERE. As your account value grows so does the aggregate amount that is being taken from your account. Over the same 10-year period with 1% in aggregate Fees (a very low estimate) one would pay 10% in fees.

So, let me get this straight, pay 10% in fees over 10 years in this example of a Mutual Fund or Variable Annuity or make a 10% bonus from day one in the Magic Annuity? Seems like a no brainer.

To some this may appear like an argument FOR investing in No Load Mutual Funds which have low fees (there is really no such thing as no fees) or invest in a No Load Index Fund linked to an index like the S&P 500. The PRIMARY difference between No Load Index Mutual Funds and the MAGIC ANNUITY are:

- The Mutual Fund does NOT PROVIDE ANY GUARANTEES ON PRINCIPAL OR MINIMUM RETURNS! YOU CAN LOSE YOUR PRINCIPAL.

- There is NO BONUS applied

- You have no personal relationship with an Advisor (that may be good).

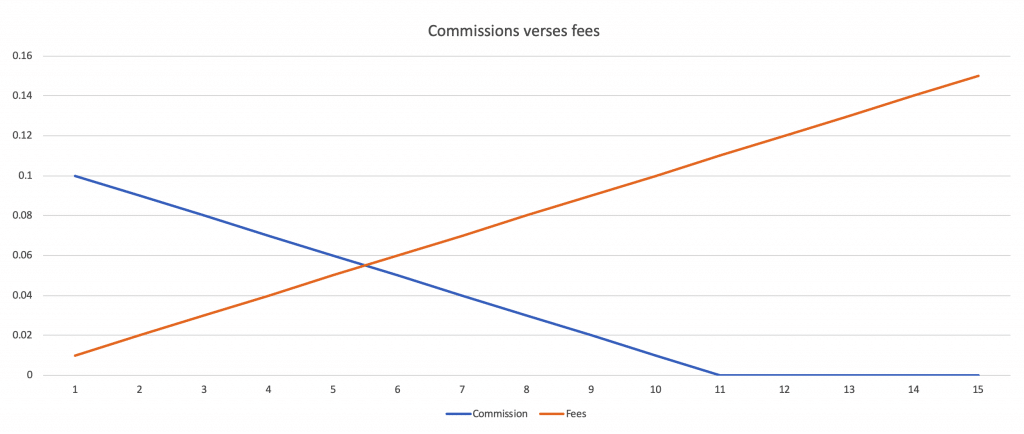

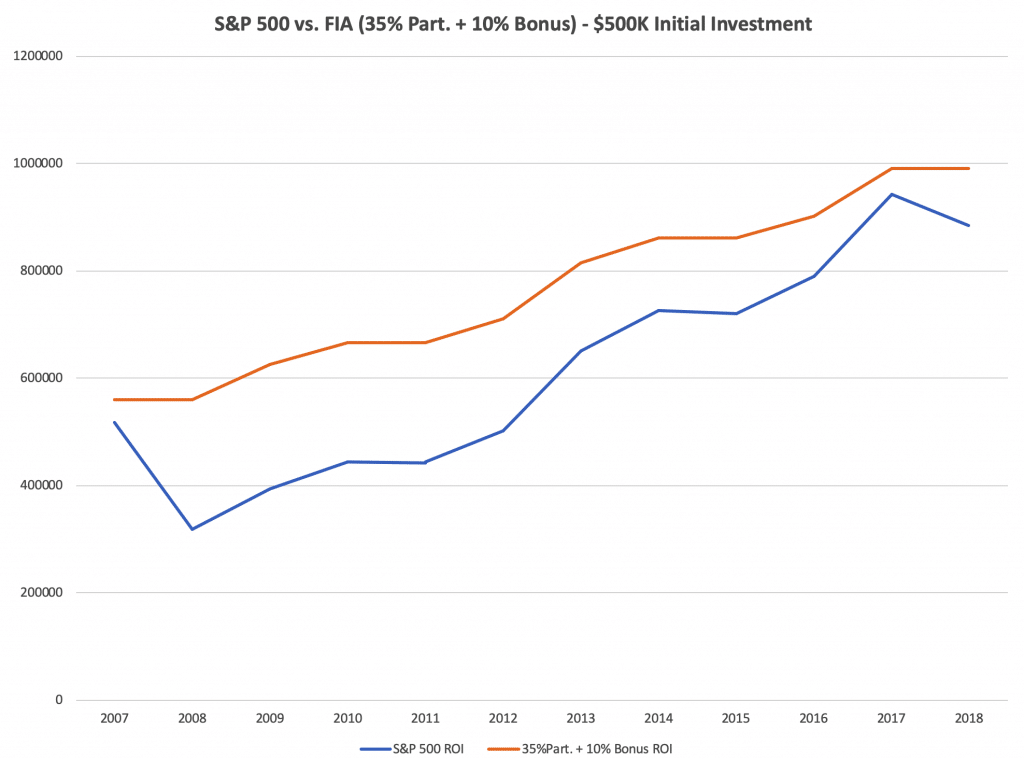

Look at this chart. It’s an example of a 5% Bonus MAGIC ANNUITY with a super long Surrender Penalty Period (10 years) and a 10% Commission, compared to an example of a 1% Assets Under Management FEE structure in a Mutual Fund or Voodoo Annuity. Over 15 years one would accumulate 15% in FEES compared to ZERO FEES and ZERO surrender penalties after 10 years in the MAGIC Annuity. Keep in mind the surrender charge which decreases over time is NEVER taken out of your account unless you liquidate early. You can see even if you liquidated after five years, you’re at break even with the fund fees, except for the BONUS YOU RECEIVED in the MAGIC ANNUITY!

Magic Annuity Returns

Now this is all fine and dandy but what kind of returns can I expect in the MAGIC ANNUITY? What kind of returns do you expect on your investments?

Would you put your life’s savings at risk for a 5% annual return? How about less?

The tough reality is that actual returns are MUCH less than investors realize for the risk involved in Variable Annuities and Mutual Fund investing.

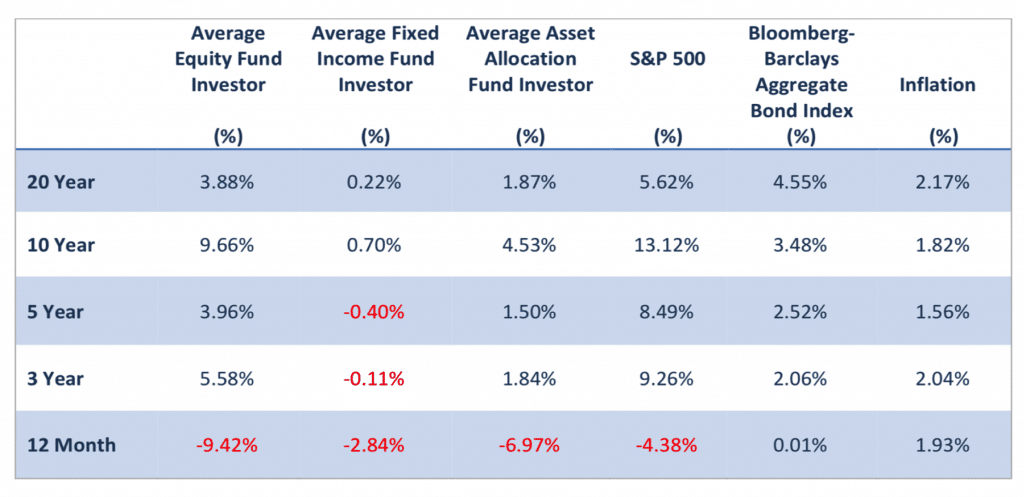

According to a new study by DALBAR, one of the financial community’s leading independent experts for unbiased ratings and performance evaluations, the typical investor in equity mutual funds has received only a 3.88% annual return… over the last 20 years!

An equity fund is a mutual fund that invests principally in stocks. It can be actively or passively (index fund) managed. Equity funds are also known as stock funds. Stock mutual funds are principally categorized according to company size, the investment style of the holdings in the portfolio and geography.

To make matters worse, when taking the 20-year average 2.17% inflation rate (a very low estimate) into consideration, the real net average annual return (increase in buying power) for the last 20 years is only 1.71%.

The study also does not account for all the fees and expenses paid out of these investment accounts to money managers and financial advisors. Even low-cost funds can charge an additional .5% and some financial advisors charge as high as 2%. Inside most Mutual Funds and Variable Annuities are the infamous 12b1 expenses which can be as high as 1.5%. Additionally, if these investments were made inside a tax-deferred account like a 401(k), 403(b), 457 (b) or IRA, about 25%-33% on average in income taxes will have to be paid, according to the Center for Retirement Research at Boston College.

Up until now we have been talking about Equity Mutual funds (and Variable Annuities – an Equity Mutual Fund inside an Annuity). These low numbers might encourage you to work with an “Advisor” who “manages” your portfolio. An asset allocation fund is a fund that provides investors with a diversified portfolio of investments across various asset classes and commonly deployed by advisors. The asset allocation of the fund can be fixed or variable among a mix of asset classes. Popular asset categories for asset allocation funds include stocks, bonds and cash equivalents.

The average investor in asset allocation mutual funds (which spread your money among a variety of classes) earned only 1.87% per year over the last two decades, but because inflation averaged 2.17% a year, they actually ended up losing 0.30% of purchasing power every year for 20 years.

The above analysis comes from the just-released 2019 Quantitative Analysis of Investor Behavior report by DALBAR, and it covers the 20-year period ending December 31, 2018.

This study concluded that…

“The results consistently show that the average investor earns less – in many cases, much

less – than mutual fund reports would suggest.”

Senator Peter Fitzgerald, Chairman of the Senate Subcommittee on Financial Management,

in a hearing about the Mutual Fund industry said,

“The mutual fund industry is now the world’s largest skimming operation,

a $7 trillion (now over $20 trillion) trough from which fund managers, brokers, and other

insiders are steadily siphoning off an excessive slice of the nation’s household, college,

and retirement savings.”

Here are a few quotes from John Bogle, the famous founder of Vanguard Mutual Funds

(The largest in the world):

“The mutual fund industry has been built, in a sense, on witchcraft.”

“On balance, the financial system subtracts value from society”

One of Wall Street’s biggest Lies is that You Must Risk Your Money in Order to Grow It.

This is simply NOT TRUE. As the famous Will Rogers once said,

“It’s not the return on my money I am worried about, it’s the return of

my money!”

Here is a chart from the above reference study showing the 20-year average returns. It speaks for itself:

The Bottom Line

The Magic Annuity Equals Higher Returns

It might help to define the MAGIC ANNUITY further. It’s called a Fixed Indexed Annuity (FIA) otherwise less known as an Equity Indexed Annuity (EIA).

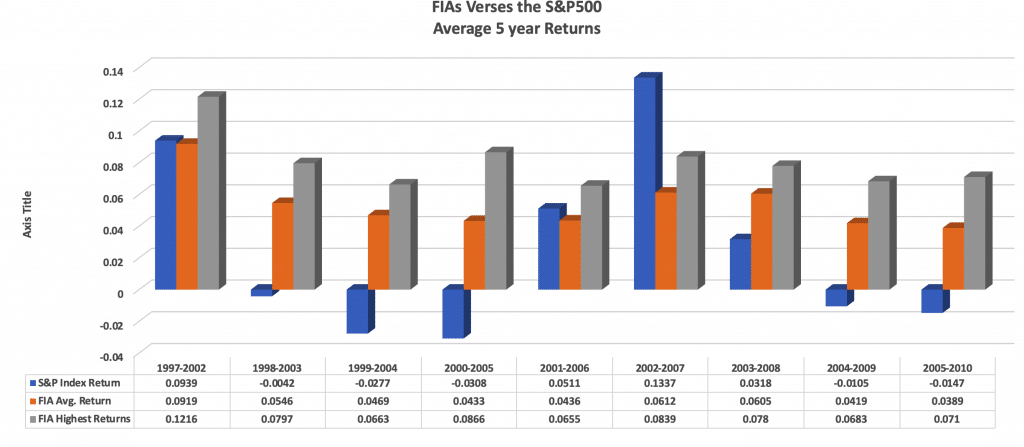

So, what kind of returns can we expect in an FIA? Before we look at the chart below, realize that these investment vehicles are just as varied as Mutual Funds and have many options, CAPS, and bonus structures to consider. Focus on the average returns as well as the highest returns, and notice some FIAs are out-performing others, but on the whole, they match or better the Mutual Fund returns without the risk.

It is important to note that the S&P had positive returns some years and negative returns in other years. While the FIA ALWAYS MADE POSITIVE RETURNS. The accumulation of only positive returns, no matter how small, has an overall cumulative effect on the portfolio.

This analysis makes a good case for the MAGIC ANNUITY, oops, FIA as a viable safe alternative to Mutual Fund and Variable Annuity investing! There simply is no reason to RISK your principal for so little upside. Alternatively, if you are investing with RISK you should be receiving a much higher rate of return.

Keep in mind that after many MARKET CORRECTIONS (MAJOR DOWNTURNS) it takes an AVERAGE OF 5 TO EVEN 6 YEARS TO RECOVER! If you are retired at or near the time of a market correction, and if you need to spend down your nest egg to cover your retirement income gap, you may never recover!

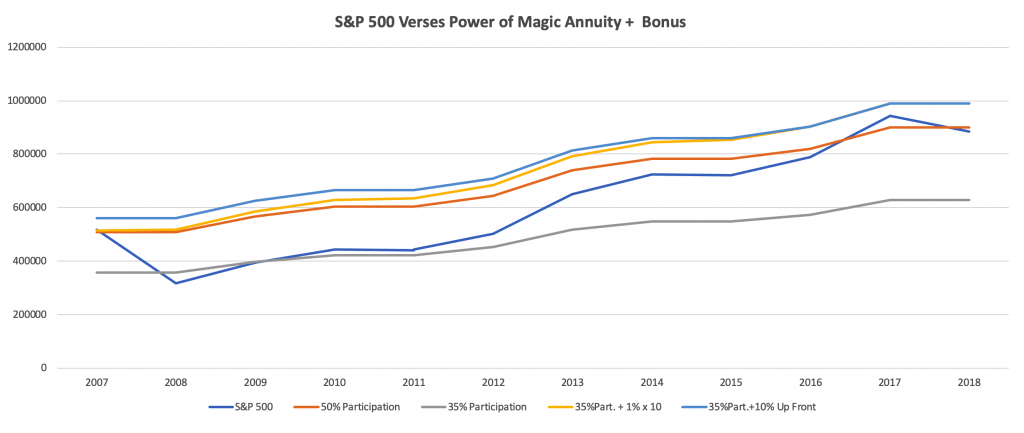

Below are my last comparison charts. Here you can see the S&P 500 (2007 – 2018) compared against an FIA that only participates in 50% of market gains, BUT None of the losses. Notice the 50% participation FIA pretty much matches the S&P over time.

Next you will see the same comparison with an FIA with an effective participation rate of only 35%. You can see the S&P easily outperforms this index investment.

Now let’s look at the effect of bonuses. If we apply a 1% bonus each year for the first 10 years, we start off tracking with the S&P but eventually surpass it. If the 10% is applied up front on the initial principal (as in the Magic Annuity), despite only participating in 35% of the upside, the BONUS FIA handily beats the S&P 500 while providing a GUARANTEE not to ever lose any money in downturns!! This is why I call it the MAGIC Annuity!

DISCLAIMER: This is not a forward-looking assessment and past performance may not be indicative of future performance. Also, All FIA’s do not have bonuses. Some bonus products pay less than 10% depending on your age. Effective participation rate in this example is a blend of CAPS and participation rates. A CAP is exactly that, a limit on how much upside is allowed.

What we do is find those FIAs where it all comes together! We work to find the MAGIC of compounding Bonuses and Effective Participation Rates. We help you find and invest in a MAGIC Annuity!

Next Steps

Please visit us at FHRI.Org and sign up for one of our FREE services:

- MAGIC Annuity evaluation and projections

- Income Retirement Gap analysis

- Pension Estimates

- A Financial Health Spectrograph – Discover the hidden risks in your portfolio

Visit FHRI.Org